Dear readers, clients and friends,

We hope you are all well. A few months ago, we posted an article on Facebook and several other social networks, regarding the abusive FLOOR CLAUSE and how Banks have been forced to repay to their clients all earnings charged in excess from “abusive” mortgages. On May 9, 2013, the Supreme Court analyzed in its ruling No. 241/2013, (in the context of a class action brought by a consumer association against several banks), the abusive character of the floor clause, declaring it null and void. However, the declaration of nullity would not affect those cases already decided by the Courts before 9 May 2013. In other words, the Supreme Court (wrongly) declared the non-retroactivity of its decision, because it would basically cause a “serious disruption to the public economic order” (in other words it was a ruling made to protect the Spanish banking sector). This erratic interpretation of the EU Law was further confirmed by another Supreme Court’s judgment of March 25, 2015.

In a nutshell, what the Supreme Court said in their two mentioned obscure Judgments was that in those cases where the existence of a floor clause had been confirmed by the Court, the Banks would be obliged to refund any interest charged in excess ONLY FROM 9 May 2013, but not retroactively to the year in which the banks began to apply floor clauses.

Luckily, a number of Spanish courts challenged before the Court of Justice of the European Union again the interpretation of the EU law made by the Supreme Court, and finally, on 21 December 2016, the Court of Justice of the European Union has recently handed down a landmark ruling (Cases C-154/15, C-307/15 and C-308/15), confirming that the Spanish Supreme Court’s 2013 decision to limit refunds to the period from May 2013 on, “failed to provide complete protection” to consumers” and subsequently, The ECJ has ordered Spain’s banks to repay all earnings from “abusive” mortgages from the year in which the banks began to apply those illegal floor clauses.

As a consequence of this recent ECJ DECISION, last 20th January 2017, the Spanish Government has finally approved a Royal Decree 1/2017, basically giving banks three months to reach agreements with customers who were offered mortgages with an abusive floor interest rate clause. As a result, the Royal Decree 1/2017 has approved several measures aimed at reaching possible out of court settlements, thereby preventing thousands of new litigants from reaching the already overloaded courts.

Subsequently, once the bank has received a letter before claim from the client’s Solicitor, it will have three months to make an offer. If an agreement is not reached within this deadline, the negotiation process will be understood to have concluded, and the client will be then able to sue the bank in Court.

However, according to the provisions of the Royal Decree-Law 1/2017, if the customer might reject the offer made by the bank and later on, he might decide to sue the bank, costs will be imposed on the bank, only if the compensation finally granted by the Court might be higher than the initial offer received from the bank.

Therefore, as litigators Solicitors, we are always mindful of alternative ways of settling disputes if possible, as it will be in our client’s best interests to pursue a satisfactory out of court settlement without litigation if possible. However, if despite all efforts, legal proceedings might have to be finally issued as a step of last resort, (if for instance the bank is intransigently opposed, we would continue to bear in mind the benefits of reaching a satisfactory out of court settlement before trial).

Our honest opinion is that the new law is very lenient with the banks. We believe that stronger penalties should be imposed on those banks that might intransigently be opposed to reach settlements. ( i.e double costs).

On the other hand, in addition to the Floor clause, we would like- if we may- to take this opportunity to inform you that the Supreme Court in its Ruling 705/2015 (dated 23th December 2015) has also declared abusive those clauses which impose on the borrower the payment of all fees, taxes and commissions associated with the mortgage loan.

Subsequently, if you are currently paying a mortgage in Spain or even if you have already paid it off up to four years ago, you may be entitled to claim, among others, a refund of the following concepts related to the Mortgage (not to the purchase of the property):

NOTARY AND LAND REGISTRY FEES, PROPERTY VALUATION COSTS, ABUSIVE COMMISSIONS, AS WELL AS THE STAMP DUTY TAX. (In total, perhaps around 2.500 Euros or more). However, bear in mind that time is of the essence, as the limitation period on order to claim these costs will expire on December 24th 2019.

In conclusion, remember if you have a mortgage and you have the suspicion that you might have serious abusive clauses in your mortgage contract, please follow the following instructions:

The first step would be to send us by e-mail your mortgage Deed as well as your latest mortgage’s monthly receipt, which will show the amount of pending capital as well as the current interest rate applied to your mortgage.

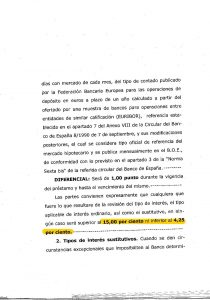

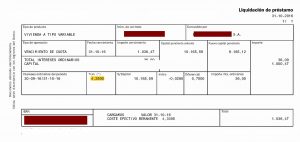

The best way to illustrate this is by giving you an example. Please see the attached photograph of a real receipt issued on-line by the bank. (Due to confidential reasons, we have obviously removed the bank’s name and our client’s personal details). However, you can clearly see highlighted in yellow, how our client has been charged last month with an outrageously high interest rate of 4,25%. Considering that the Euribor now is -0,070 %, the impact of this abusive floor clause in our client’s case is VERY SIGNIFICANT. The other attached document is an extract of a real mortgage Deed, containing a very abusive ceiling-floor clause.

In the second place, should you be affected by any of these above mentioned abusive clauses in your mortgage, – as a prior step, – we always recommend entering into correspondence or friendly negotiation with the bank. The negotiation process will aim to reach a satisfactory out of court settlement, saving the time and costs involved in protracted litigation. However, it is important that you DO NOT ACCEPT ANY PRESSURE FROM THE BANK. All banks are losing the court cases, so it is in their best interest to reach an amicable agreement with you, offering the best possible financial terms and conditions. Likewise, remember NEVER TO NEGOTIATE WITH OUR BANK ON YOUR OWN AND DO NOT SIGN ANY AGREEMENT, unless an independent qualified Solicitor-like our Firm-has already verified very carefully the content as well as the legal and financial implications of the proposed agreement in the long term.

In conclusion, there is very little that is “standard” in these kinds of mortgage contracts and agreements signed with banks, making it especially important that you know exactly what you’re agreeing to. That’s why, in matters of such complexity and importance where a lot of money is at stake, it is vital that you seek the right professional, – only a qualified registered Lawyer, – in order to give you the most adequate professional advice.

“Ricor Abogados&Solicitors” has a strong legal team with proven extensive experience in all areas of law. We run an independent and cost effective Law Firm helping hundreds of clients across a range of legal services in Spain, from corporate and individual civil and criminal litigation, and we are proficient in dealing with banks with regards to the removal of abusive clauses from mortgage contracts.

Our high rate of success is subsequently explained by the fact that we continually provide complete and “home-made” tailored solutions to individuals and businesses alike. If you kindly check our testimonials section of our website www.ricorabogados.com, you will find plenty of testimonials from real clients who put their trust in our Firm and they are all now all extremely grateful to our Firm for the excellent work and legal protection offered, which fills us with a lot of professional pride.

Therefore, should be interested in receiving specific advice regarding this matter (or any other legal issue), please do not hesitate to send us an e-mail to: ricorsolicitors@yahoo.co.uk, and we will be most delighted to be of assistance to you. Alternatively, you can also know more about our services by logging to our website www.ricorabogados.com.

Thank you very much again for your attention and we look forward to giving you a personalized service and the benefit of a high quality and cost effective advice.

Kindest regards

Mr. Oscar Ricor Morales

“NON-PRACTISING ENGLISH SOLICITOR IN ENGLAND AND WALES”, under the “Solicitors Regulation Authority” (SRA) SRA number 519196 and practicing Spanish Solicitor.

Other Articles